Will we cross the chasm in 2025?

A cautiously optimistic view on the year to come.

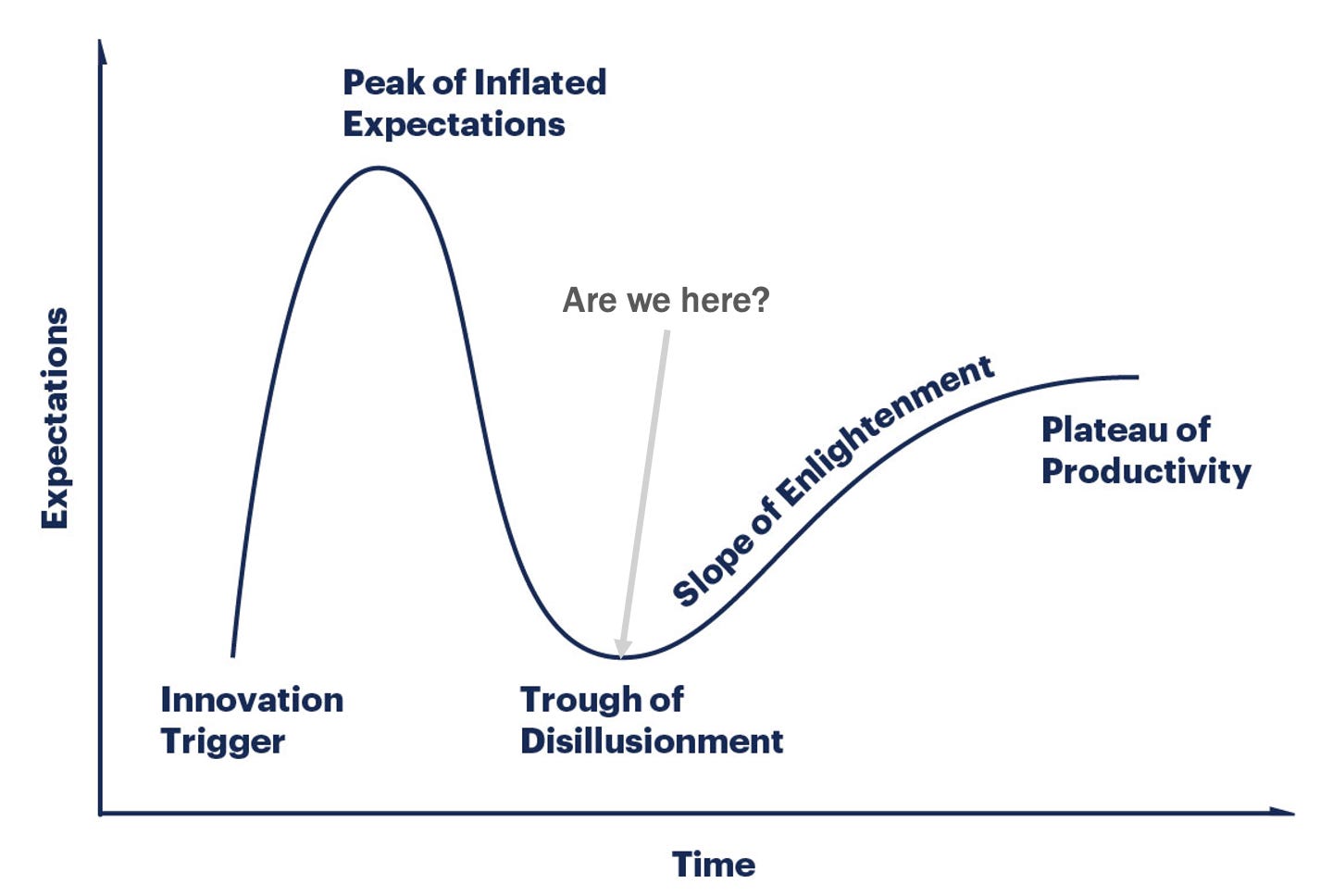

For those familiar with innovation theory, 2024 felt a little like the pit of desillusionment for the sustainability community. But, as always, the year brought a mix of challenges and glimmers of hope, offering clues on the trends which may shape 2025.

To get some perspectives on how to make sense of 2024, and what we should both expect and focus on in 2025, I reached out to John Atcheson from CircularWay, Isabelle Lefort from Paris Good Fashion, Lewis Perkins from the Apparel Impact Institute, Nic Gorini from Spin Ventures, and Pascal Brun from Zalando to get their insights!

From a high level, they point towards the need for pragmatism, concrete solutions and tangible outcomes. Specifically, their answers helped identify a few trends for 2025: towards a course correction on policy, bridging the funding and innovation gap, and rebuilding trust and alignment across stakeholders.

Please note that the below is informed by the responses of the consulted expert but does not represent their opinion.

Policy: towards course correction?

2024 Recap

For numerous European companies, the cost of compliance went through the roof this year, and many were surprised by the resource intensity and cost of leading EU regulations like the CSRD. A key aspect of this comes from the support of consultants and technology companies in meeting regulatory requirements.

This mobilisation of resource and budgets has had two adverse consequences:

It reinforced boards’ perspective that sustainability is expensive and without ROI at a time where budgets are often constrained.

It limited the ability to advance actual mitigation or adaptation work by the teams.

2025 Trend

While no one questions the importance of regulations in driving and aligning industry action, there is a need to strike a balance to avoid overburdening companies with bureaucratic demands.

Last year, we discussed the opportunity to focus on “policies that demonstrate how the green transition can contribute to local economic development and job creation”. There are emerging signs that European leaders may be reconsidering their approach, moving towards a less business sceptic and more innovation driven strategy. This shift may be primed by the learnings from the “The Future of European Competitiveness” led by Mario Draghi. For instance, Wopke Hoekstra, the European Commissioner for Climate, Net Zero and Clean Growth, acknowledged to Bloomberg last week that ““we have been too one-dimensional […] And therefore it is so important that we invest way more into the competitiveness side.”

We also mentioned the potential for the EU to develop their own version of the IRA. Could 2025 be the year it comes to life? Signs such as the collaboration between the European Investment Bank and the Societe Generale to unlock €8 billion in investments supporting manufacturers across the wind energy supply chain in Europe suggest it might just be.

Open Questions

How will a climate sceptic and isolationist US government, who threatened to pull out of the UNFCCC entirely, affect global regulatory and investment dynamics in sustainability?

How will policymakers navigate the tension between the growing demands for action from communities experiencing the devastating impact of climate change, and the fatigue many constituents feel towards highly constraining climate regulations?

Bridging the funding and innovation gap

2024 Recap

Last year, we highlighted the risk of economic tightening for innovators and the opportunity for collective derisking. As forecasted, the economic context of 2024 significantly influenced investment strategies, away from exponential growth, towards quality growth and proven paths to profitability. This made it more challenging for novel approaches or pre-revenue companies to secure funding. In addition, the maturing green technology space saw investors becoming more pragmatic, placing greater emphasis on understanding actual demand and process scalability.

Collective derisking approaches also faced challenges, with many private companies remaining hesitant to embrace blended capital models. Despite this resistance, these models began to demonstrate their potential, particularly in renewable energy investments within supply chains.

2025 Trends

There will be significant opportunities for innovative solutions in 2025, but they won’t be evenly distributed, requiring thoughtful considerations to unlock their full potential, with a few key topics likely to grow in importance.

First, circular solutions like waste to value - whether in closed loops for batteries or textiles, or in open loops from agri-food to textiles - and regenerative practices will gain in interest. However, this interest will be coupled with more realism around the systems approach needed to scale these solutions, and particularly the need for specialised expertise and infrastructure. Increased investments in upskilling and public-private partnership will likely play an important role in the development of the core infrastructure necessary for the commercial viability of circular systems.

Second, decoupling strategies are set to make their way to the boardroom, with more companies exploring what “less but better” approaches could mean for them. This shift will not necessarily be driven by sustainability alone, but as a reaction to evolving consumer markets where fatigue and product saturation are becoming more apparent, leading to slower growth. These dynamics will encourage brands to explore new models that balance financial performance with reduced resource intensity.

Actions to advance these priorities will be more focused and targeted than before, moving away from big picture statements. Instead, the emphasis will shift to answer the critical question: what can truly make a material difference in the medium term from both a business and sustainability perspectives?

Open Questions

Who pays for sustainability? Suppliers, brands, governments, customers? Everyone in some way? As scaling sustainable solutions in a commercially viable way becomes a priority, this question will be highly contentious and likely condition many outcomes.

How willing will companies be to explore new development pathways? Can they recognise that tried and proven approaches are showing signs of exhaustion and embrace innovative alternatives?

Rebuilding trust and alignment across stakeholders

2024 Recap

One thing became clear in 2024: the ambition to use sustainability and circular economy as a means to align stakeholders across industry and policy needs more work. Policymakers, particularly in Europe, expressed frustration with the lack of progress made by corporates, while tensions emerged within industries over who should bear the cost of transitioning to greener supply chains.

Within companies, board-level interest in sustainability decreased, with many viewing it as costly and disconnected from immediate business needs. Heavy investments in compliance, combined with mixed results from some sustainability innovation programmes, have led business leaders to demand clearer ROI.

Customer behaviour in 2024 continued to expose deep contradictions. While surveys continue to indicate that consumers care about sustainability and claim they are willing to pay more for sustainable options, their spending habits often contradict this. Few actively consult transparency pages, and their purchasing decisions continue to favour cheaper, faster alternatives.

This inconsistency is exacerbated by a decline in trust towards institutions and brands, polarisation on major issues, and a fatigue with the relentless product and information flow. In this saturated, commodified landscape, many products and brands have lost their unique value, becoming interchangeable or reduced to mere memes.

2025 Trends

To address these growing misalignments, 2025 will see a stronger focus on aligning stakeholders through projects that balance business impact with sustainability. Initiatives will need to demonstrate concrete, measurable business outcomes to gain support. The same expectations will apply to supply chain greening efforts, with stakeholders seeking tangible benefits before committing further investments or engagement.

Leaders will need to adopt a dual focus: maintaining a long-term vision and ambition for sustainability - such as 25-year decarbonisation or regeneration goals - while delivering shorter-term projects that build trust and achieve meaningful results within 5 years or less. Expect increased investment in scalable circular systems and supply chain transparency, driven by regulations and innovations in lifecycle assessments and traceability.

To onboard customers in circular solutions, brands must fully integrate these systems rather than offering half-hearted initiatives. Consumers want to feel part of an innovative, dynamic ecosystem - not like experimental participants in clumsy model. Successful circular solutions will be seamless, trustworthy, and fully integrated into the brand experience.

As dissatisfaction with declining product quality and unmet brand promises continues to grow, customers will increasingly focus on the perceived and delivered value of products. This shift will favour brands that offer durable, high-quality goods alongside transparent, meaningful engagement around their sustainability efforts.

Open Questions

Will the politisation of every issue start to fade as more and more communities experience the tangible impacts of climate change?

Will we see the emergence of visionary leaders, willing to venture in uncharted territories to create transformative business and environmental opportunities?